Buy Now, Pay Later (BNPL) – What is it?

A buy now, pay later (BNPL) plan is a loan provided to a consumer at the point of sale to enable them to make an online purchase without using a credit card. Popular choices include Amazon, Affirm, after pay, Sizzle, PayPal, and Klarna’s Shop Pay Installments. A point-of-sale loan is often funded after many lenders do an instant soft credit check on the customer (the kind that doesn’t affect your credit score). Customers have a variety of alternatives for repaying the loan balance, depending on the firm they hired and the amount borrowed; some payment options carry interest, others do not, and other businesses impose late fees or fees for missed payments. BUY NOW PAY LATER firms may levy a cost to the merchant to compensate for the lack of interest charged to the consumer.

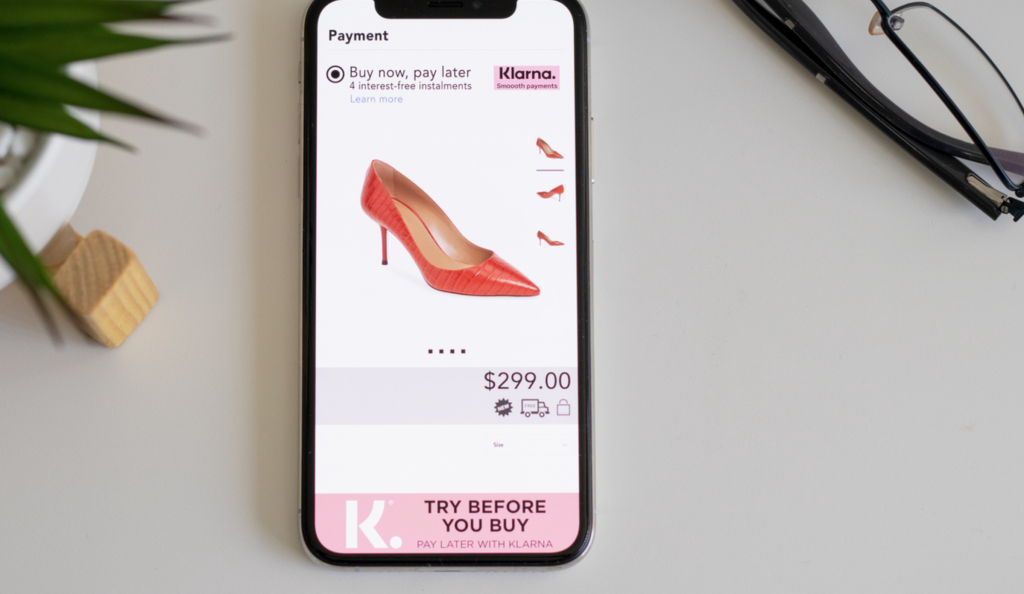

How does buy now pay later works?

Here is how consumers and retailers can use the BUY NOW PAY LATER process.

- Continually making purchases, a customer starts the checkout process. If you’re a customer, you begin the buy now pay later procedure just like any other online purchase. You browse your preferred online retailers, make your selections, and get ready to pay.

- A buy-now-pay-later option is provided by the retailer’s chosen buy-now-pay later vendor. The consumer will have the choice to purchase using buy now pay later throughout the checkout process, in addition to other options like credit or debit cards.

- The lender performs a mild credit inquiry on the borrower. When a customer chooses to pay using BNPL, they provide certain personal information to the buy-now-pay-later lenders, such as a full address and social security number. In order to ensure that the borrower would eventually repay their loan based on their credit history, the lender performs a mild credit check on them right away. Since this form of credit check is not submitted to credit agencies, credit scores won’t be negatively impacted as they may be due to a full credit check.

- The retailer pays a fee to the vendor. The merchant is charged directly for the percentage of the retail transaction that the BNPL vendor retains. The buy-now-pay-later lender deducts the fee from the amount they send to the merchant (which usually ranges between 2% and 8%). This is comparable to the agreements established between traditional credit card providers and merchants.

- The client settles the balance over time. If a customer pays their entire bill within a short period of time, the majority of BNPL vendors provide interest-free payments, typically for 30 days. Lenders provide a variety of payment options with various interest rates if clients need extra time to pay off their bills. Similar to using a credit card, a consumer pays less overall interest the quicker they pay off their balance.

Buy Now, Pay Later – Consumer Benefits

- It serves as a leveler for individuals without credit cards.

- Adaptable payment choices.

- Payment options that do not charge interest.

- No harm is done to your credit via soft credit checks.

Conclusion

You will need to strike a balance between two factors as a shop thinking about the BNPL option. One is the cost that BNPL vendors add to each transaction. The other is the rise in the number of shopping carts used by clients of BNPL services.

The majority of BNPL shops do not make their merchant fees available to the public. However, they normally fall between 2% and 8% of a customer’s total purchase price. They now compete with big credit card issuers as a result. Because of this, offering BNPL services might not cost a business any more than offering credit card services. Additionally, buy now pay later services may encourage clients to make larger purchases, much like credit cards do. Retailers including Macy’s, Peloton, and Rue21 have reported significantly higher sales from customers using buy now pay later services. For many additional businesses and those mentioned above, the increased sales volume makes up for the costs they are paying.